What I Learned About Taxes When My Business Crashed

When my business failed, I thought the worst was over—until the tax bill hit. I felt overwhelmed, confused, and completely unprepared. Looking back, I realize tax compliance wasn’t just a formality; it was a lifeline. The collapse of my company left me emotionally drained and financially exposed, but nothing compared to the shock of receiving notices from the IRS months after I thought everything was finished. I had assumed that closing the doors meant the end of obligations. I was wrong. Unfiled returns, unpaid payroll taxes, and unreported asset sales came back to haunt me. In this guide, I’ll walk you through what I wish I’d known earlier: how to protect yourself, stay compliant, and avoid costly mistakes when your business falls apart. This isn’t just about rules and forms—it’s about responsibility, clarity, and the quiet strength it takes to face the aftermath with honesty and purpose.

The Wake-Up Call: Facing Reality After Business Failure

The first year after my business closed was one of the most difficult of my life. I had invested over seven years and nearly every dollar I had saved into building a small retail operation that specialized in handmade home goods. For a time, it thrived. We had loyal customers, a steady cash flow, and a small team I considered family. But when supply chain disruptions and declining foot traffic hit, we couldn’t adapt fast enough. The day I locked the store for the last time, I felt a mix of grief and relief. Grief for what had been, and relief that the daily stress was over. I thought the hardest part was behind me.

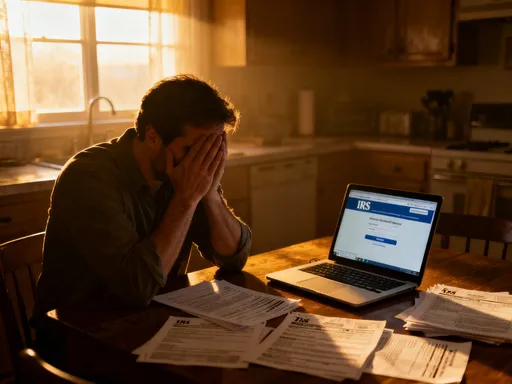

It wasn’t. Three months later, I received a letter from the state tax authority. Then another from the IRS. They weren’t asking for updates—they were demanding payment. I hadn’t filed a final income tax return for the business. I hadn’t settled the last quarter’s payroll taxes. I hadn’t reported the sale of equipment. In my mind, the business was dead, so those responsibilities were too. But the government doesn’t operate on assumptions. To them, my business still existed on paper, and its obligations hadn’t vanished with the sign in the window. The penalties began to accumulate quickly, and with no income coming in, the pressure was unbearable. I felt trapped by a system I didn’t understand, and worse, by my own ignorance.

This experience taught me that business failure isn’t a single event—it’s a process. And one of the most critical phases happens after the doors close. Emotionally, it’s tempting to walk away and never look back. But financially and legally, walking away without resolution can be devastating. The tax consequences of an improperly closed business can follow you for years, affecting your credit, your ability to start again, and even your personal assets. I wasn’t alone in this. Studies show that a significant number of small business owners fail to file final tax returns or settle outstanding liabilities after closure, often due to confusion or fear. But ignoring the problem only makes it worse. The wake-up call for me wasn’t just the letters—it was the realization that responsibility doesn’t end when the dream does.

Why Tax Compliance Still Matters When You’re Shutting Down

One of the most dangerous misconceptions among small business owners is that once a business stops operating, all tax duties end. This couldn’t be further from the truth. Tax compliance remains essential, even in dissolution. The Internal Revenue Service and state tax agencies require specific actions when a business closes, and failing to meet these obligations can result in serious consequences. These aren’t just bureaucratic hurdles—they are legal requirements designed to ensure accountability and prevent tax evasion. Understanding what compliance looks like after shutdown is the first step toward protecting yourself.

First, you must file a final income tax return for the business. This return covers the period from the beginning of the tax year to the date the business ceased operations. It’s not optional. Even if the business earned no income during that final stretch, the return must be filed. For sole proprietors, this means completing Schedule C as part of their personal tax return. For corporations or partnerships, separate final returns are required. These documents inform the IRS that the business is no longer active and provide a clear endpoint for reporting.

Second, payroll tax obligations must be settled. If you had employees, you were responsible for withholding federal income tax, Social Security, and Medicare taxes from their wages. These funds are held in trust for the government, and failure to remit them can lead to what’s known as the Trust Fund Recovery Penalty. This penalty can be assessed against the business owner personally, meaning your home, savings, or wages could be at risk. I didn’t realize this at the time, but the unpaid payroll taxes from my last two payrolls were not just a business debt—they were a personal liability.

Third, sales tax must be reconciled. If your business sold taxable goods or services, you collected sales tax from customers with the promise to forward it to the state. Even if the business is closed, that obligation remains. States have no statute of limitations on unremitted sales tax in many cases, and audits can occur years later. Additionally, if you sold business assets—equipment, inventory, furniture—you may need to report those transactions and pay taxes on any gain. All of these steps are part of responsible closure. Compliance isn’t about perfection; it’s about honesty. It’s about closing the chapter properly so you can start a new one without the weight of unresolved debt.

Sorting the Mess: Organizing Records When Everything Feels Broken

After the closure, my office was a disaster. Boxes of invoices, stacks of bank statements, and years of disorganized digital files made the idea of sorting anything feel impossible. I was emotionally drained, and the thought of facing that mountain of paperwork was paralyzing. But I knew that without records, I couldn’t file accurate returns or respond to tax notices. I had to start somewhere. The process wasn’t neat, but it was necessary. Over several weeks, I developed a system that helped me regain control—one that didn’t require perfection, just progress.

The first step was identifying the most critical documents. I made a list: bank statements for the past three years, all 1099s and W-2s issued, copies of previous tax returns, sales records, and any correspondence from tax agencies. I didn’t need every receipt—just enough to reconstruct income, expenses, and tax payments. I sorted them into categories: income, expenses, payroll, assets, and liabilities. Physical documents went into labeled folders. Digital files were moved into clearly named folders on my computer and backed up to an external drive. I didn’t worry about missing items at first; the goal was to create a working foundation.

Next, I reached out to my bank and credit card providers to request electronic statements. Many financial institutions keep records for up to seven years, so even if I had lost my copies, I could retrieve them. I also contacted my accountant, who still had copies of past returns and some supporting documents. Having a professional on my side made a huge difference. They helped me identify gaps and advised me on how to estimate figures when exact records were missing. The IRS allows for reasonable reconstruction of records, especially in cases of hardship, as long as the effort is made in good faith.

What I learned is that organization doesn’t require everything to be perfect. It requires intention. You don’t need every scrap of paper to file a final return—you need a clear picture of what happened. By focusing on key documents and seeking help when needed, I was able to compile enough information to move forward. The process wasn’t fast, but it was empowering. Each folder I labeled, each statement I uploaded, was a step toward resolution. And in the midst of failure, that sense of progress was invaluable.

Talking to the IRS (Without Losing Your Cool)

Calling the IRS used to terrify me. I imagined angry voices, endless hold times, and automatic penalties. When I finally picked up the phone, I was shaking. But what I found surprised me. The representative I spoke with was calm, professional, and willing to listen. She didn’t judge me for my situation. Instead, she asked questions, reviewed my account, and explained my options. That conversation didn’t erase my debt, but it gave me something even more important: clarity. I learned that the IRS isn’t your enemy—they’re a government agency with rules, and those rules include provisions for people in financial distress.

One of the most important things I discovered was the possibility of an installment agreement. Because I couldn’t pay my tax bill in full, I applied for a payment plan. This allowed me to settle the debt over time with manageable monthly payments. There is a setup fee, and interest continues to accrue, but it’s far better than ignoring the bill and risking a lien or levy. I also learned about the Offer in Compromise program, which allows taxpayers to settle for less than the full amount if they can prove financial hardship. While I didn’t qualify, knowing it existed gave me hope that options were available.

Communication is key. The worst thing you can do is stay silent. The IRS would rather work with you than pursue collection actions. When I called, I made sure to document everything—dates, names, reference numbers, and summaries of conversations. I kept copies of all letters and forms. I also requested written confirmation of any agreements. This paper trail protected me and ensured accountability on both sides. If you’re overwhelmed, you can authorize a tax professional to speak on your behalf using Form 2848. Having an expert handle the details can reduce stress and improve outcomes.

The lesson here is simple: don’t wait. If you owe money, reach out early. Explain your situation honestly. Ask questions. Be polite but persistent. The IRS has systems in place to help taxpayers in hardship, but you have to engage. Silence leads to penalties, wage garnishments, and bank levies. Cooperation leads to solutions. I wish I had called months earlier. The earlier you act, the more control you have.

Cutting Losses the Smart Way: Deducting What You Can

One of the few bright spots in my business failure was the realization that some of my losses could actually reduce my tax burden. I had always thought of deductions as tools for profitable businesses, but they also apply in times of loss. The IRS allows business owners to deduct legitimate business expenses, and when a business closes, certain losses can be claimed on personal tax returns. This doesn’t erase the pain of failure, but it can ease the financial blow if handled correctly.

For example, I was able to claim a net operating loss (NOL) for the year my business closed. An NOL occurs when business deductions exceed income. Under current tax rules, I could carry that loss back to previous years to recover some of the taxes I had paid, or carry it forward to offset future income. This provided some relief, especially since I had income from a new job the following year. I also deducted the cost of unsold inventory that had no resale value. When I sold equipment for less than I paid, I reported those losses as well. Even unpaid debts from customers—known as bad debts—could be written off if I could prove they were previously included in income.

But there are rules. Not every loss qualifies. Personal expenses, even if paid through the business, aren’t deductible. And the IRS watches for red flags, like excessive deductions in the year of closure. To avoid scrutiny, I made sure every claim was supported by documentation. I kept records of purchase prices, sale receipts, and efforts to collect unpaid invoices. I also consulted my tax advisor before filing. Timing mattered too. Filing an accurate, complete return early helped me avoid penalties and positioned me to claim benefits without delay.

This experience taught me that failure doesn’t have to be financially catastrophic. With careful planning and honest reporting, you can turn some losses into tax advantages. It’s not about gaming the system—it’s about using the rules to your benefit. Every dollar saved on taxes is a dollar that stays in your pocket, helping you rebuild. I didn’t recover everything, but I recovered more than I would have if I’d given up.

Protecting Yourself: Separating Business and Personal Liability

One of my biggest regrets was how closely I blended my personal and business finances. I used my personal credit card for business purchases. I paid personal bills from the business account. I didn’t keep separate records. At the time, it seemed easier. But when the business failed, that lack of separation put my personal assets at risk. I didn’t realize that by blurring the lines, I was potentially exposing my home, car, and savings to creditors and tax authorities. The legal protection offered by structures like LLCs or corporations only works if you maintain a clear distinction between personal and business affairs.

When you form a legal business entity, it creates a separate legal identity. This means the business, not you personally, is liable for its debts—under normal circumstances. But if you treat the business as an extension of yourself, courts can “pierce the corporate veil” and hold you personally responsible. This is more likely when records are poor, funds are mixed, or formalities like annual filings are ignored. In my case, because I hadn’t maintained clean accounting or filed final reports, I lost some of that protection. The IRS pursued me personally for unpaid payroll taxes, and I had no strong defense.

Now, I understand the importance of discipline. Business income goes into a business account. Business expenses are paid from that account. Personal spending comes from personal funds. I also make sure to file all required reports on time, even if the business isn’t active. When I eventually close any business, I will formally dissolve the entity with the state, cancel the EIN with the IRS, and close all related accounts. These steps may seem minor, but they’re essential for closing the loop and protecting my future.

Separating finances isn’t just about legality—it’s about mindset. It reinforces the idea that a business is a distinct venture, not an extension of your identity. This clarity makes decision-making easier and reduces emotional entanglement. It also builds credibility with banks, vendors, and tax authorities. If I ever start another business, I’ll do it right from day one. Clean records, clear boundaries, and consistent compliance aren’t just best practices—they’re forms of self-respect.

Starting Over: Building a Tax-Smart Mindset for the Future

Today, I run a smaller, more sustainable business. It doesn’t have the grand ambitions of my first venture, but it’s stable, well-organized, and tax-compliant from the start. The failure of my first business was painful, but it taught me lessons I couldn’t have learned any other way. I now see tax compliance not as a burden, but as a form of self-protection. It’s not about fear of punishment—it’s about respect for the system and responsibility to myself.

I file returns on time, even when there’s no income. I keep digital and physical records organized. I communicate with tax authorities proactively, not reactively. I consult professionals when I’m unsure. These habits didn’t come naturally, but they’ve become second nature. They’ve given me peace of mind and financial resilience. I’m no longer afraid of the IRS because I know I’m doing my part.

To anyone facing the aftermath of business failure, I want to say this: you are not alone, and you are not defined by this moment. The path forward isn’t easy, but it is possible. Start by facing the facts. Gather your records. Make the phone call. File the return. Take one step at a time. Responsibility today builds freedom tomorrow. I’ve learned that true strength isn’t in avoiding failure—it’s in how you respond to it. And sometimes, the most powerful response is simply to do the right thing, even when no one is watching.